Market Intelligence

Understanding the Numbers: AHRI Shipment Report Breakdown for March 2024

June 6, 2024 | 3 minute read

Encouraging outlooks came with the AHRI March 2024 Shipment Report:

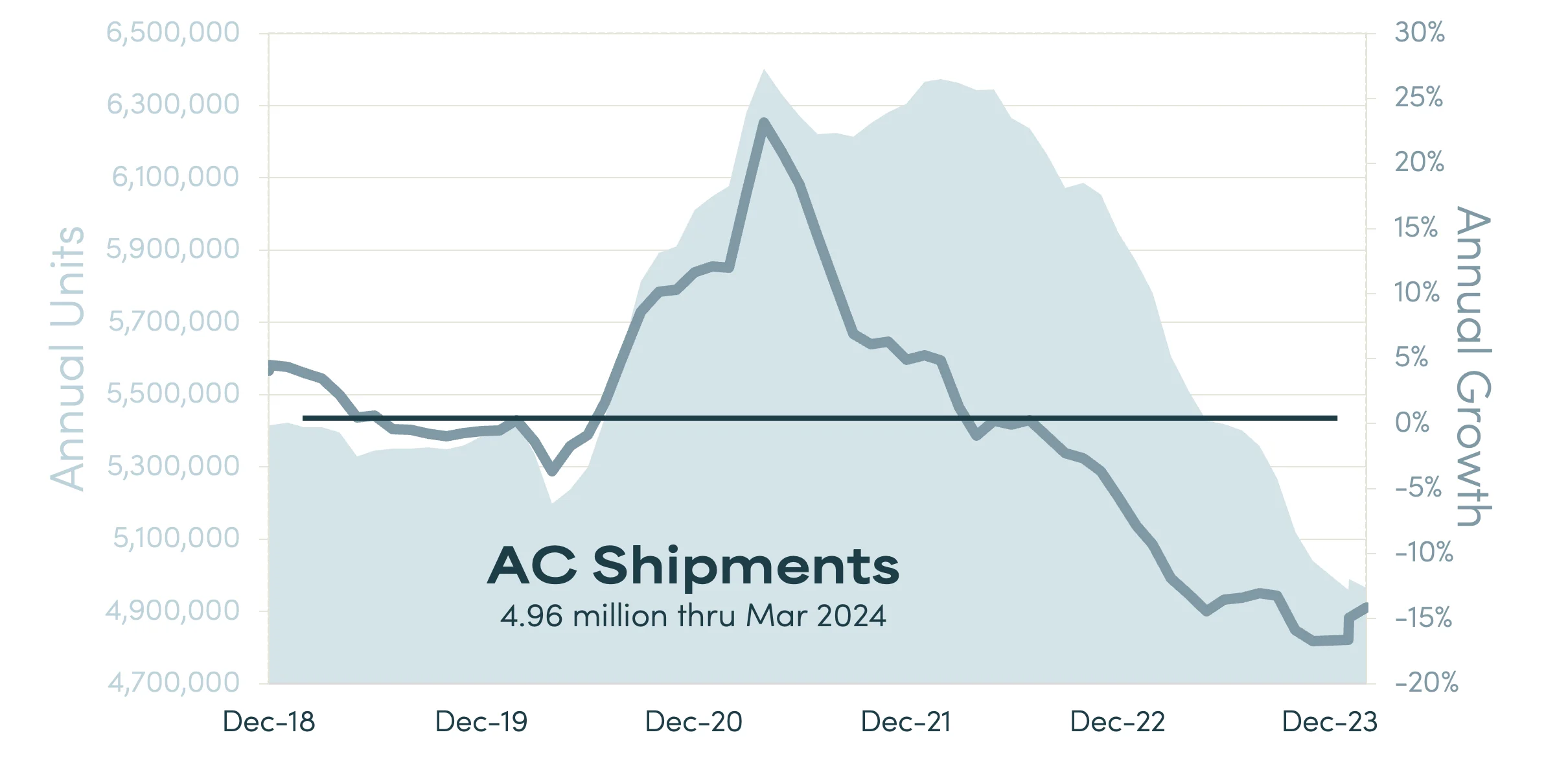

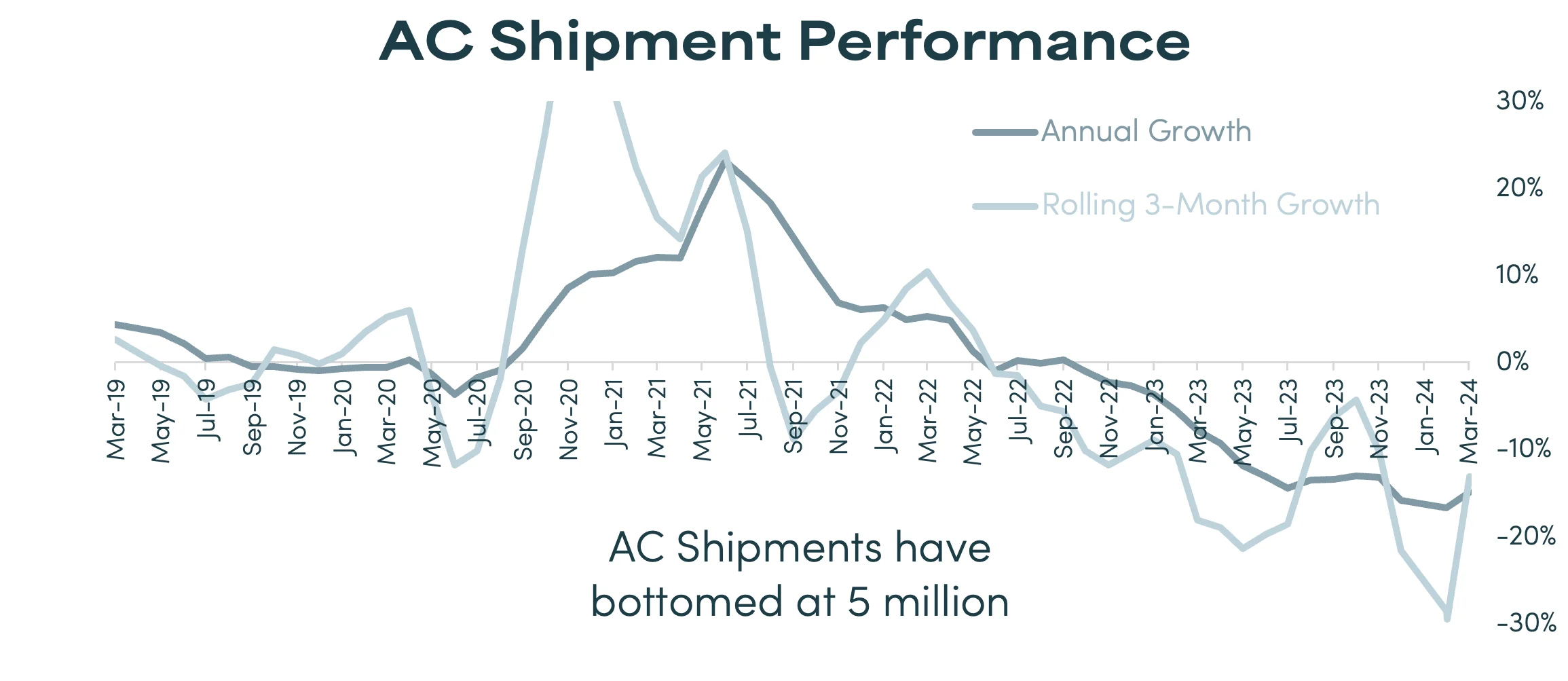

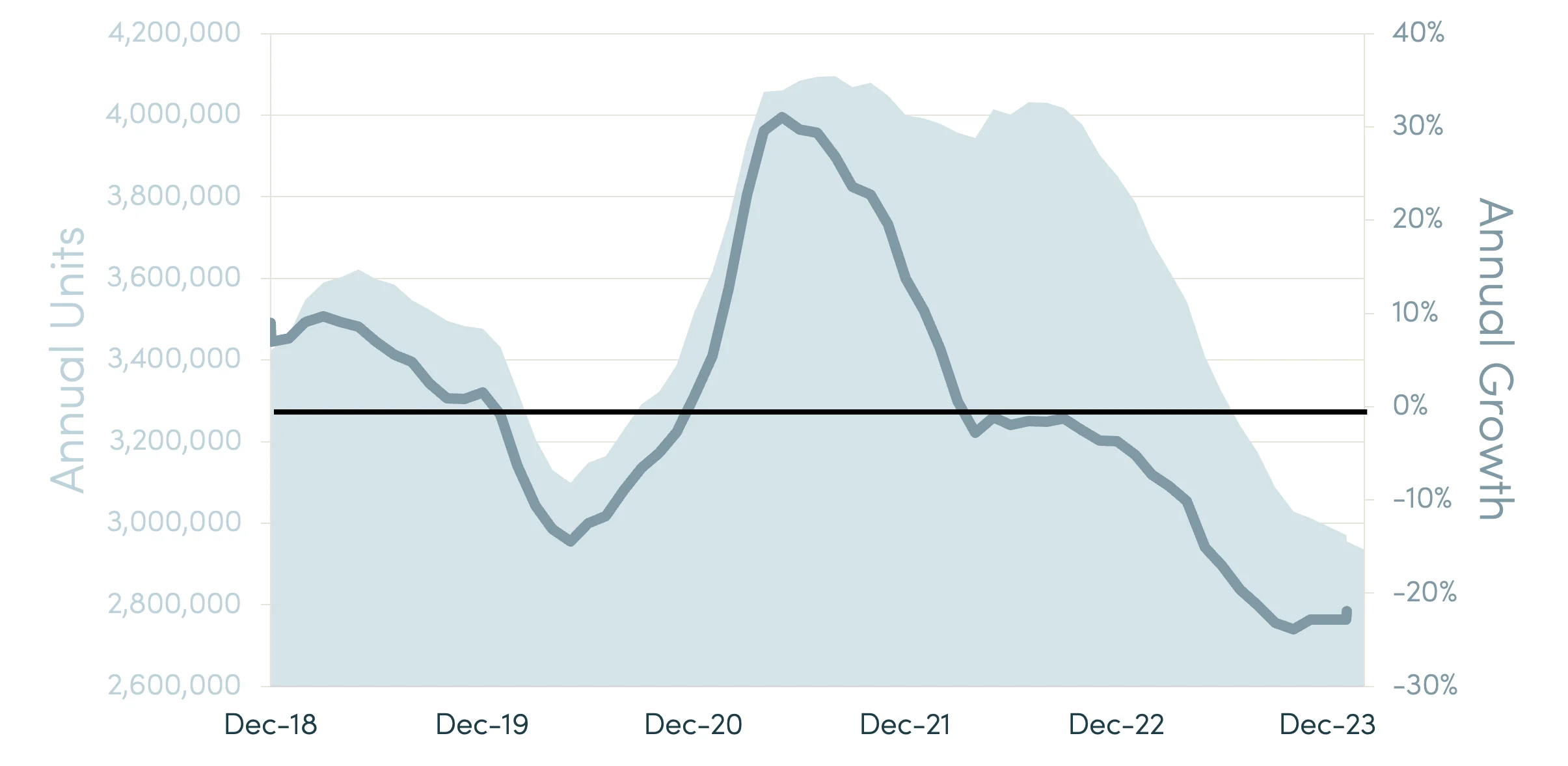

Air conditioner shipments bottomed at 5 million.

Air conditioner shipment performance may look gloomy at first glance until you look forward through 2024. There were 470.7K air conditioners shipped during March 2024, a decline of 5.2% from March the previous year. The 3-year average for AC shipments decreased by 14.8%. The total number of AC shipments over the past 12 months amounts to 4.96 million, which is off by -14.1% from one year ago. Year-to-date AC shipments show a decline of 6.4%. For ACs, March typically represents 9.4% of total annual shipments, which implies a current rate of 5.033 million, or 1.4% up from the last 12 months. March and February combined typically represent 15.1% of total annual AC shipments, implying a current shipment rate of 5.59 million or a 12.5% increase from the last 12 months.

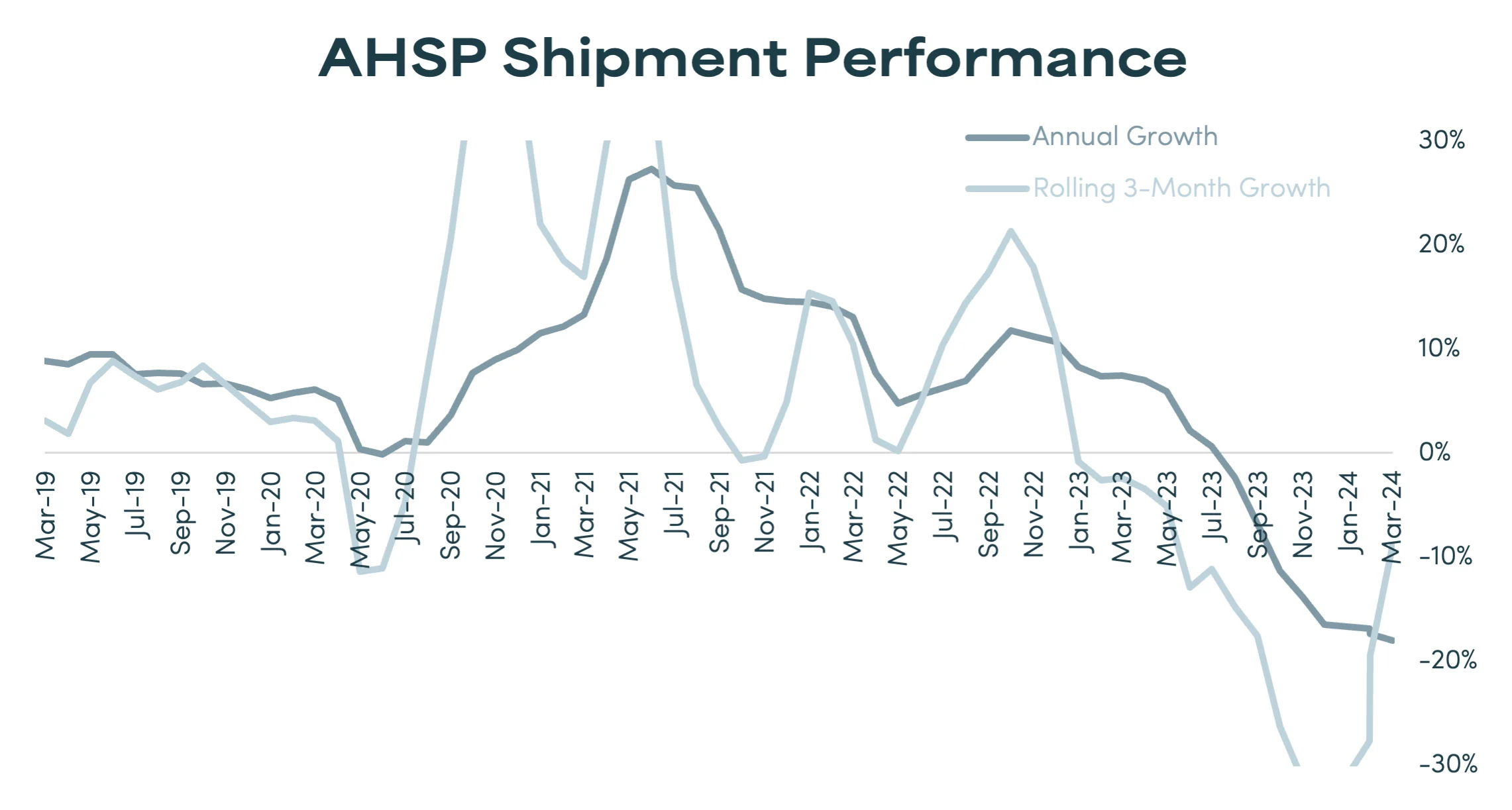

Heat Pump Shipments Flat

There were 368K Heat Pumps shipped during March 2024, a decline of 3.5% from March 2023. The 3-year average for heat pump shipments increased by 1%. The total number of heat pump shipments over the past 12 months amounts to 3.53 million, which is off by -18.1% from the 12 months through March 2023. Year-to-date heat pump shipments show a decline of 8.9%. For heat pumps, March typically represents 10% of total annual shipments, which implies a current rate of 3.67 million, or 3.9% up from the last 12 months. March and February combined typically represent 16.9% of total annual heat pump shipments, implying a current shipment rate of 3.85 million or a 9.1% increase from the last 12 months.

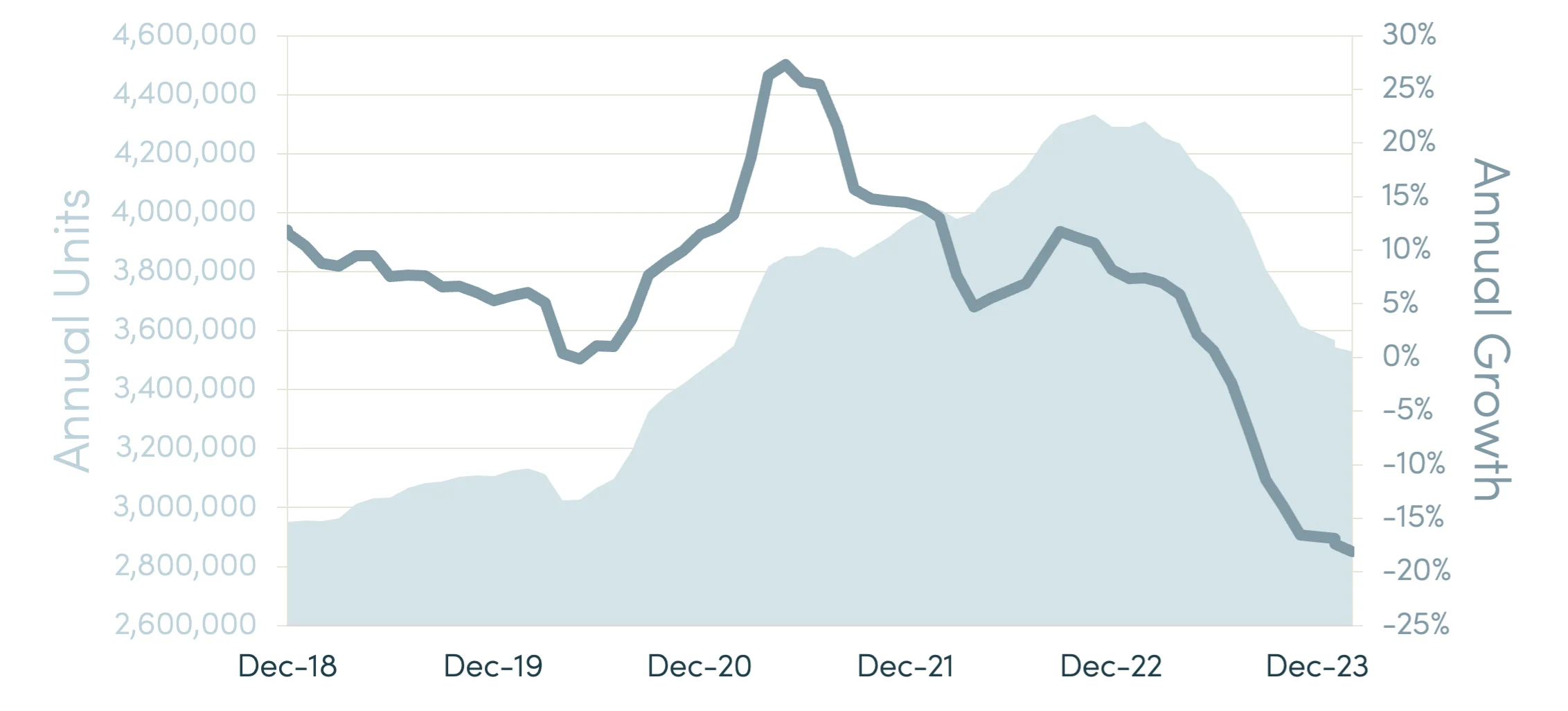

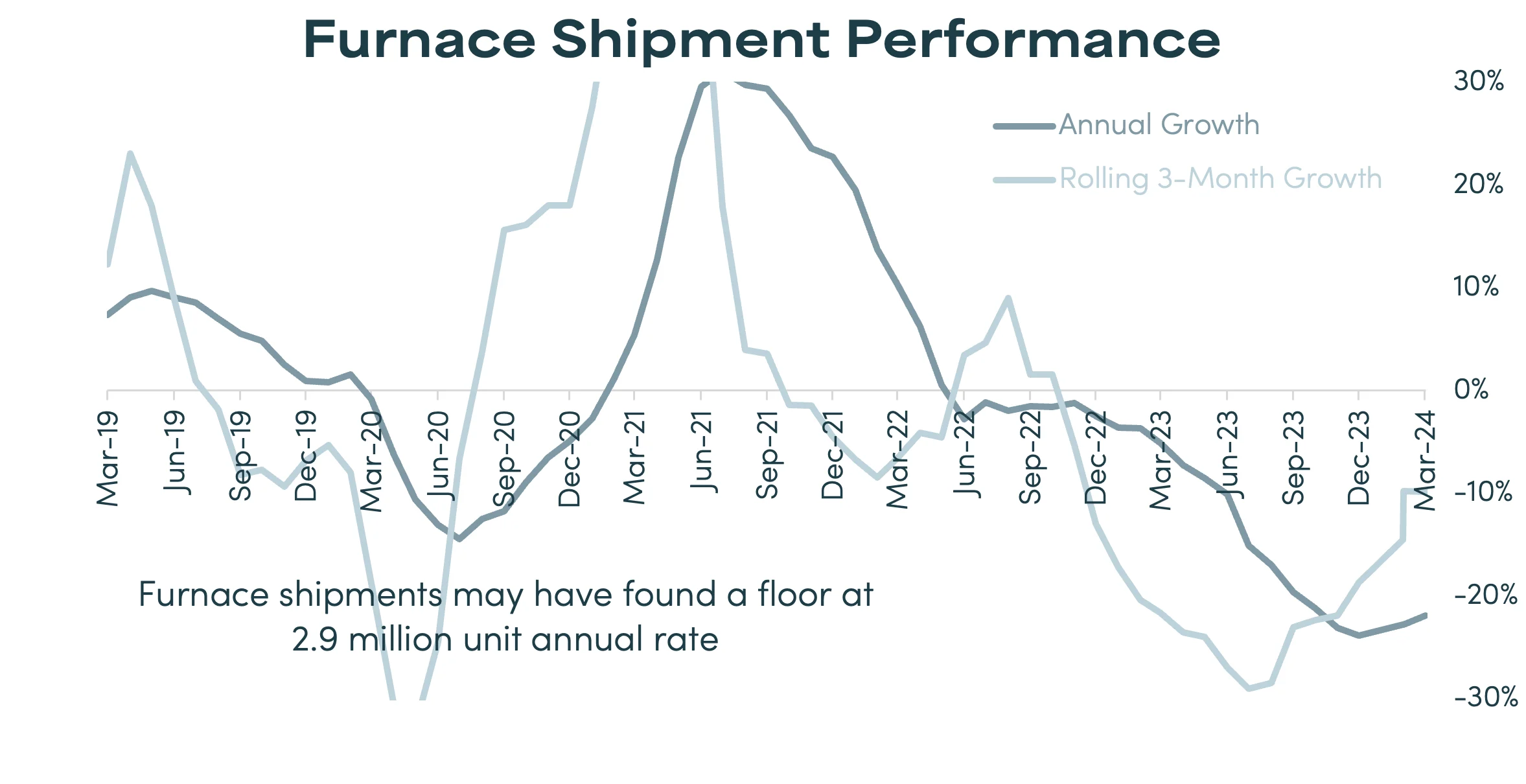

Furnace Shipments Found the Floor

During March 2024, there were 250.4K furnace shipments (a combination of natural gas and oil), a decline of 7% from March the previous year. March 2024 furnace shipments were -25.6% lower than the recent 3-year average for shipments for March. Over the last year, furnace shipments totaled 2.94 million, down by 20.4% from March 2023. Year-to-date furnace shipments have declined by 9.9% through March 2024. March 2023 typically represents 7.8% of total annual shipments, implying a current rate of 3.22 million, or 9.5% up from the last 12 months. March and February combined typically represent 14.2 % of total annual shipments, implying a current shipment rate of 3.25 million, or 10.8% up from the last 12 months.

HARDI distributors over the past four years managed sales growth near zero at the arrival of Covid, up to 25%, and now back to zero. The trend back to zero highlights the “normalization” process we endured in 2023. The historic normal or median annual sales growth is around 6% and around 2.5% for price increases. These trends will continue to settle into a more normal pattern during 2024.

Since 2021, distributors nationwide have observed a 5-percentage point decline in AC sales relative to their total sales of ACs, ASHPs, and furnaces. This decline has primarily benefited heat pumps, although furnace sales have also gained market share despite a sluggish market. How has your product mix shifted?

Learn More About Unitary Product Movement

The AHRI Shipment Report tracks units sold into the channel, but by participating in HARDI’s Unitary Report, distributors can learn exactly what products are moving across different U.S. states and regions, measured by product type and efficiency level.Please contact Tim Fisher or Grace Helser if you are interested in participating!

Grace Helser

Distribution Market Analyst

As a Research Analyst on HARDI's Market Intelligence team, Grace leverages her education in business and economics from the Ohio State University to provide industry insights and benchmarking programs for HARDI membership. She has a strong foundation in analysis and statistical methods, which she utilizes through in-depth survey work to develop comprehensive membership insights.